Conversational AI

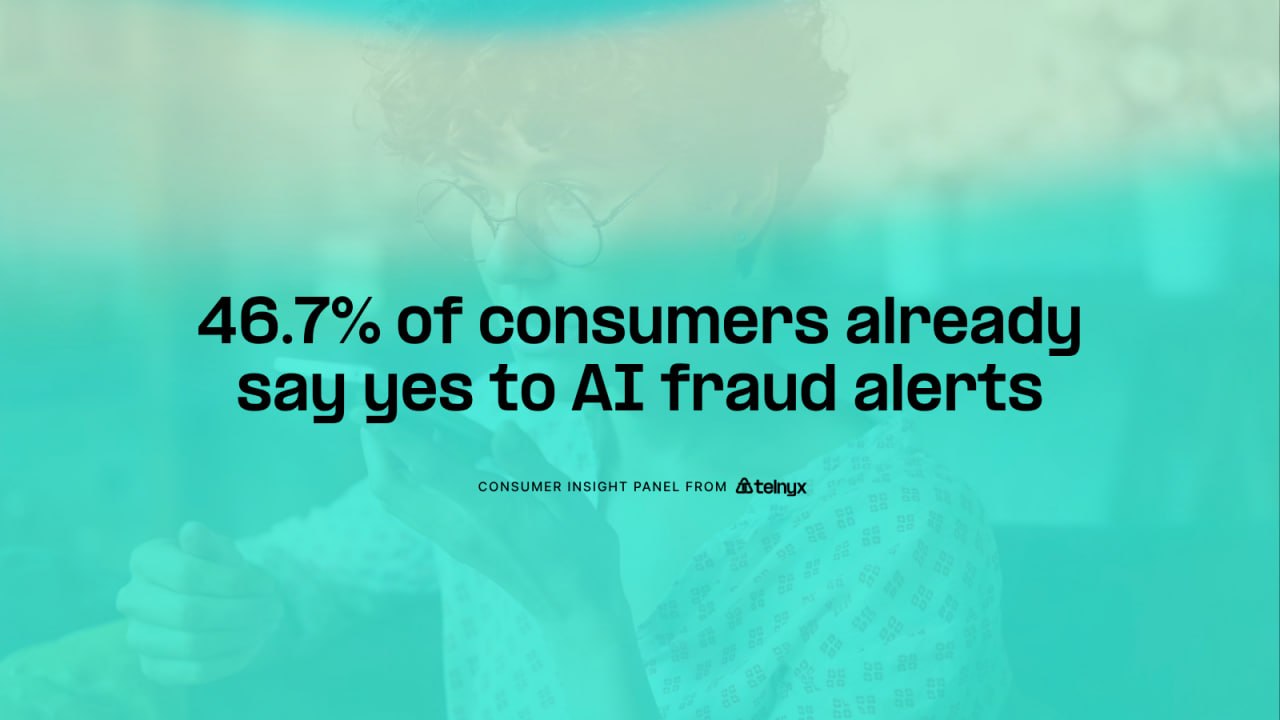

Consumer Data: Nearly Half Already Say Yes to Voice AI Fraud Alerts

By Telnyx Expert Team

Key findings:

- 46.7% would answer a Voice AI fraud call to confirm or reject a suspicious transaction, the only question where agreement exceeds disagreement

- 31.4% prefer voice login over passwords, but 48.6% disagree

- Trust drops sharply as tasks shift from reactive (fraud alerts) to advisory (recommendations) and autonomous (applications)

- Only 27.6% prefer applying for financial products via Voice AI over forms, the lowest agreement in the survey

- The data reveals a trust gradient: urgency drives acceptance, delegation faces resistance

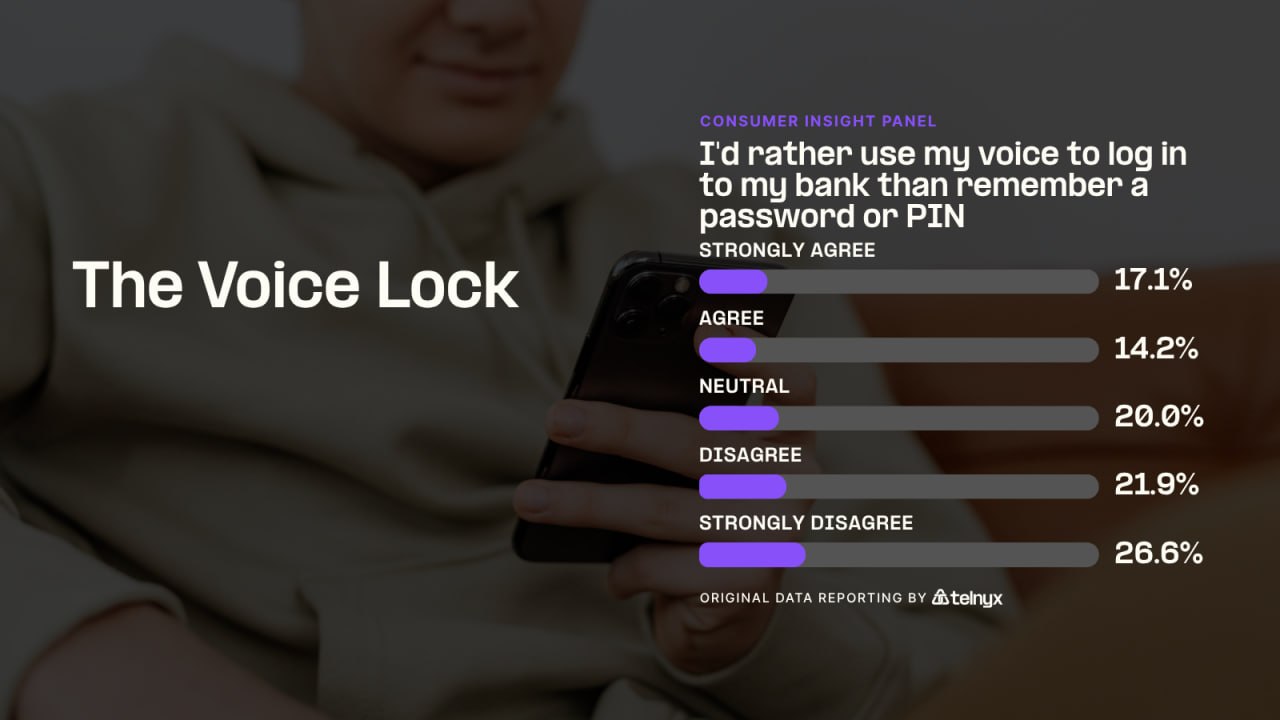

The Voice Lock

I'd rather use my voice to log in to my bank than remember a password or PIN.

31.4% of respondents prefer voice authentication over passwords or PINs, but nearly half (48.6%) disagree. The split suggests password fatigue alone is not enough to drive voice login adoption. Consumers may acknowledge that passwords are frustrating while still distrusting biometric alternatives, particularly for financial access where a compromised login has immediate monetary consequences.

The 20% neutral response is worth noting: these respondents have not formed a strong opinion either way. For banks, this represents a persuadable middle. A voice login experience that is demonstrably secure and faster than a password reset flow could move the neutral bloc toward adoption. Without that proof point, the default remains skepticism.

The disagreement pattern is notable because voice login is the lowest-stakes question in the survey. If consumers resist AI for authentication, the barrier only climbs from here. Banks deploying Voice AI agents for login may need to pair it with visible security signals, such as branded caller ID or multi-factor verification, to overcome the trust deficit.

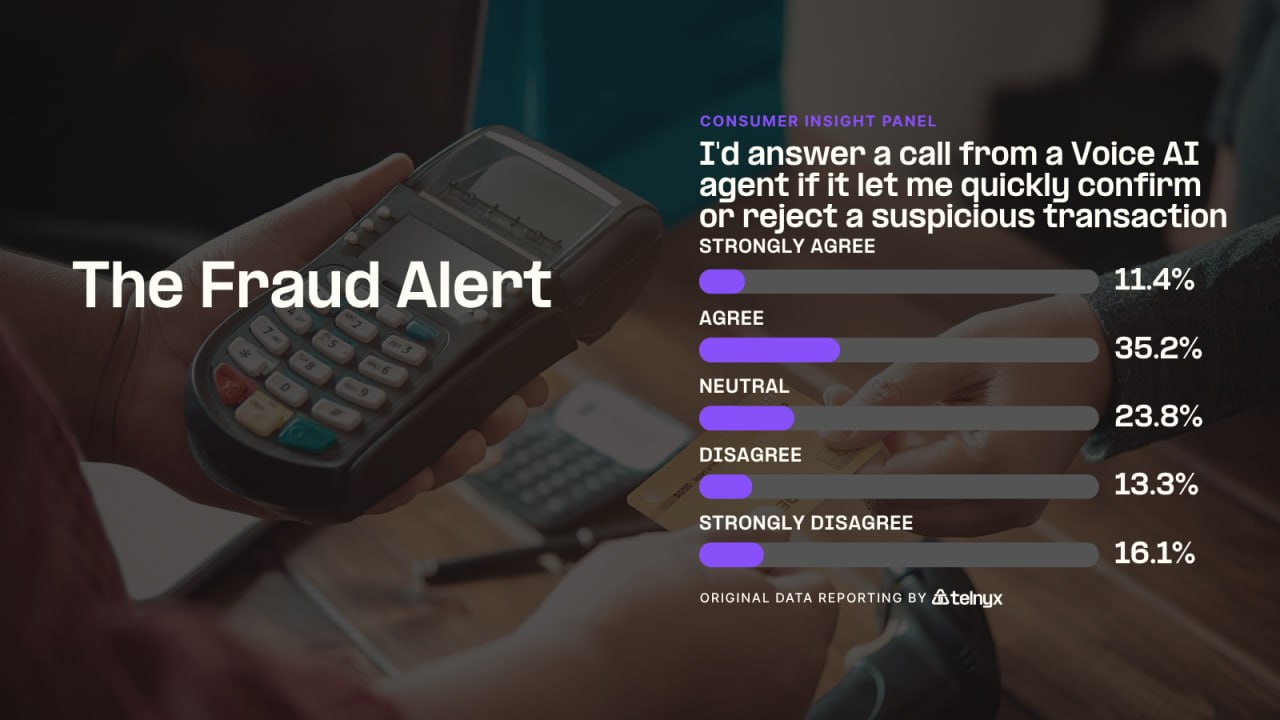

The Fraud Alert

I'd answer a call from a Voice AI agent if it let me quickly confirm or reject a suspicious transaction.

This is the only question in the survey where agreement (46.7%) exceeds disagreement (29.5%). Fraud alert calls benefit from a dynamic that other banking tasks do not: urgency. When a suspicious transaction appears, speed matters more than channel preference. Consumers who would never answer an AI call for a balance check will pick up for a fraud alert because the cost of ignoring it is real and immediate.

The 35.2% who agree (not strongly) suggests a pragmatic middle: they are not enthusiastic about AI, but they recognize the utility when the alternative is finding a fraud notification buried in an app or waiting for a human agent to call back. The 11.4% who strongly agree likely represent consumers who have already experienced the frustration of delayed fraud response.

The 29.5% who disagree may reflect robocall fatigue and voice phishing concerns. Banks deploying AI fraud calls face a credibility problem: the same technology that enables legitimate fraud alerts also enables the spoofing attacks that make consumers distrustful of unsolicited calls. Branded calling and STIR/SHAKEN attestation are not optional for this use case. They are prerequisites. Without verified caller identity, AI fraud alerts risk being ignored by the very customers who need them most.

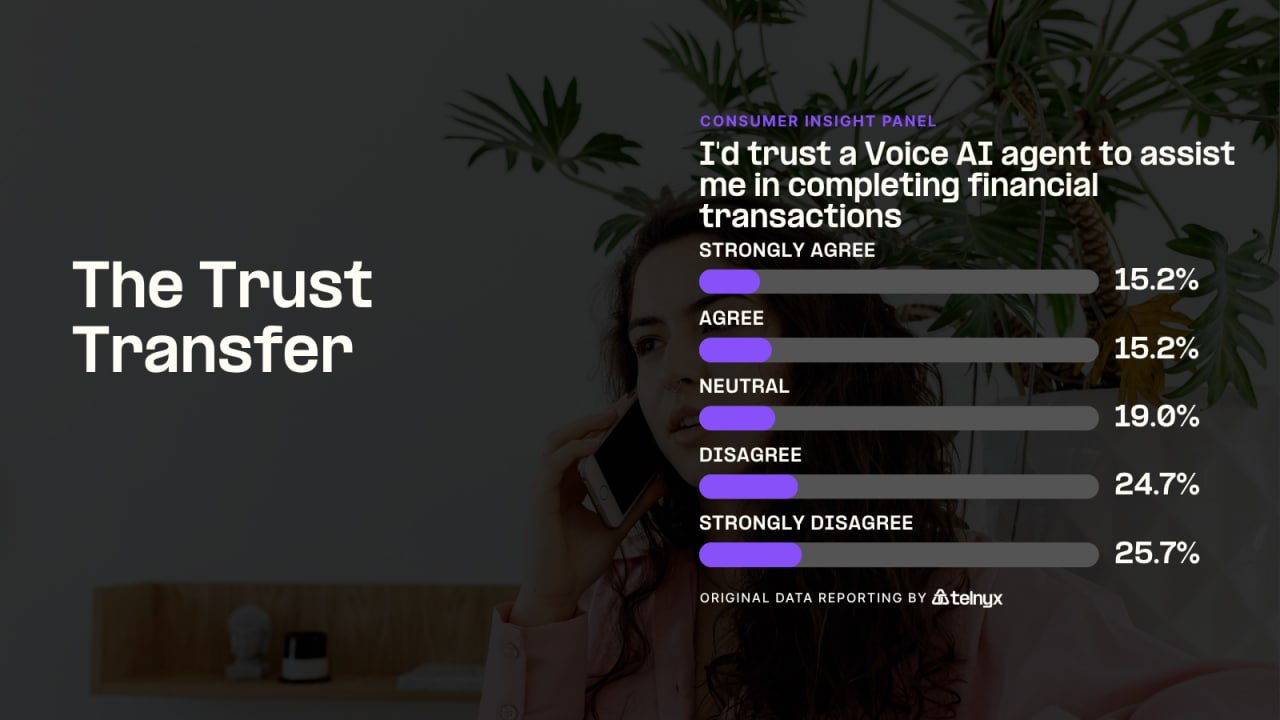

The Trust Transfer

I'd trust a Voice AI agent to assist me in completing financial transactions like bill payments, balance checks, and transfers.

Agreement drops to 30.5%, and disagreement crosses the majority threshold at 50.5%. This is the inflection point in the survey: the moment where consumers move from "AI could help me" to "AI should not be doing this."

The shift from fraud alerts (46.7% agree) to transaction assistance (30.5% agree) represents a 16-percentage-point drop. The difference is not capability. Consumers do not doubt that AI can process a bill payment. The resistance is about error correction and accountability. If a fraud alert is wrong, you ignore it. If a bill payment is wrong, you are out real money and chasing a resolution through customer service. The stakes are asymmetric, and consumers know it.

The near-even split between strong disagree (25.7%) and disagree (24.8%) suggests a consistent block of resistance rather than a polarized minority. These are not respondents on the fence. They have decided, and their decision is no.

For banks, the implication is clear: Voice AI for transactions must include explicit confirmation flows, read-backs, and undo mechanisms. The interaction design cannot assume trust. It must earn it at every step, starting with speech-to-text accuracy that eliminates the most common failure mode: AI mishearing a dollar amount or account number.

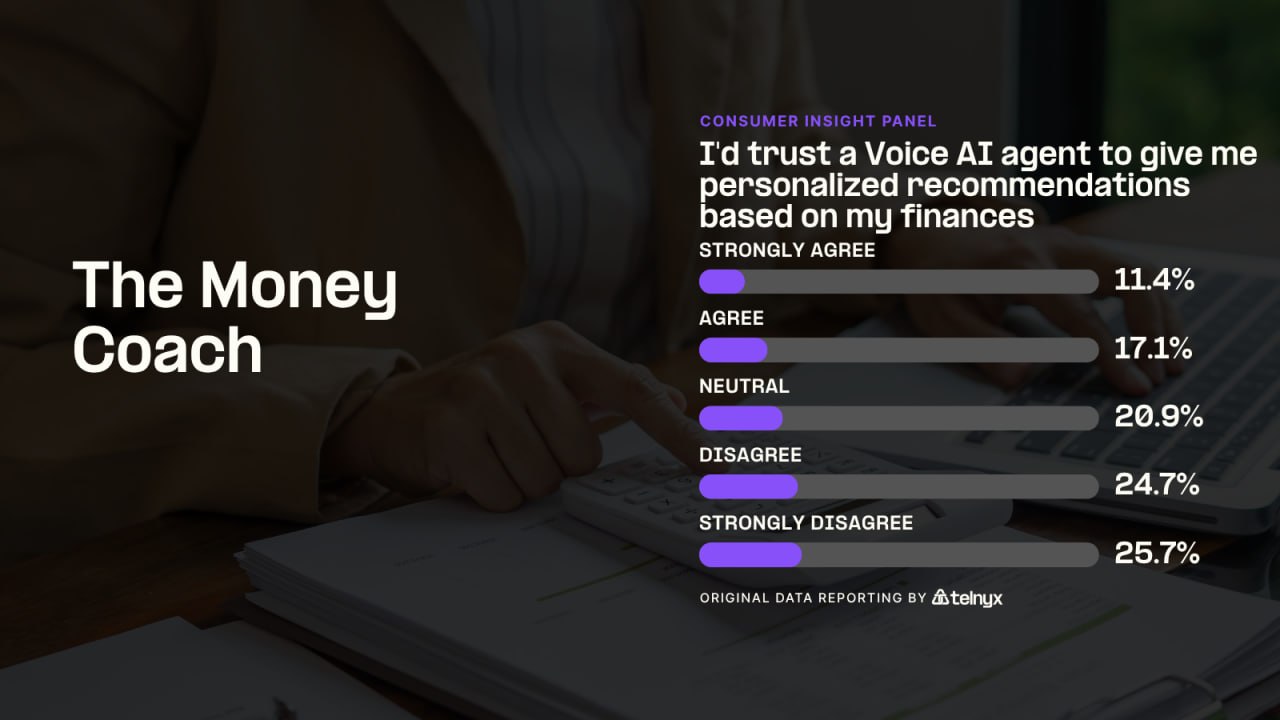

The Money Coach

I'd trust a Voice AI agent to give me personalized recommendations based on my finances.

Only 28.6% trust Voice AI for personalized financial recommendations, while 50.5% disagree. The agreement rate barely moves from the transaction question (30.5%), but the nature of the resistance shifts. Transaction skepticism is about errors. Recommendation skepticism is about motives.

When AI suggests a financial product, consumers ask a question that does not arise in fraud alerts or bill payments: who benefits from this recommendation? If the AI suggests a high-yield savings account, is that the best option for the customer or the most profitable one for the bank? Algorithmic opacity fuels the doubt. Consumers cannot inspect the recommendation logic, and they know it.

The 20.9% neutral response is the highest in the survey for any question outside voice login. These respondents have not rejected AI recommendations outright. They are waiting for proof that the system works in their interest. Banks that can demonstrate transparent recommendation logic, third-party audited algorithms, or clear conflict-of-interest disclosures may be able to move this group. Those that cannot will find the 50.5% disagreement rate hard to overcome.

The practical takeaway: Voice AI in banking should not lead with recommendations. Lead with tasks where the AI's interests and the customer's interests are clearly aligned (fraud alerts, balance checks), then expand to recommendations only after trust is established through consistent, error-free interactions.

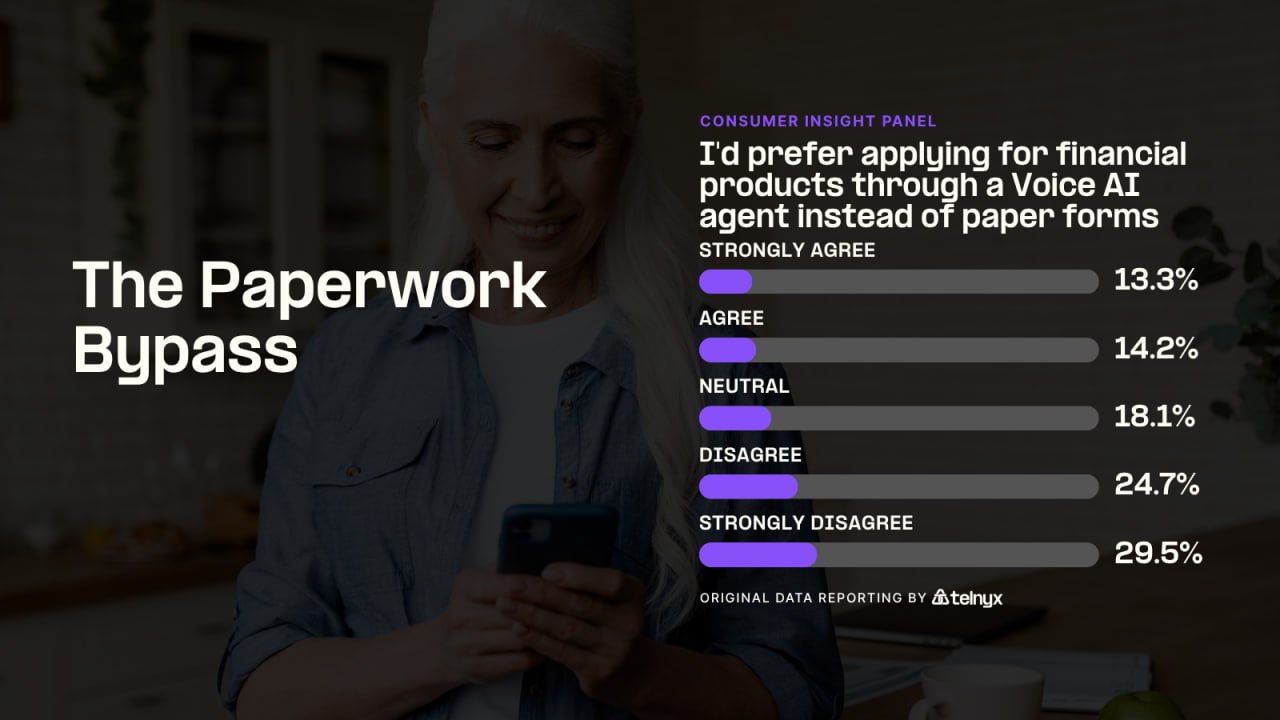

The Paperwork Bypass

I'd prefer applying for financial products through a Voice AI agent instead of filling out paper or online forms.

This hits the lowest agreement in the survey at 27.6% and the highest disagreement at 54.3%. Financial product applications are where Voice AI acceptance hits its floor. The resistance combines every trust barrier from the previous questions and adds a new one: deliberation time.

Applying for a credit card, loan, or insurance policy is a consequential financial commitment. Consumers want to read terms, compare options, and take time before committing. Voice is inherently ephemeral. You cannot scroll back through a conversation to re-read an interest rate. You cannot bookmark a verbal disclosure to review later. The medium works against the task.

The 29.5% who strongly disagree is the highest in the entire survey. These respondents are not just skeptical. They are actively opposed to the idea, likely because voice feels like a high-pressure sales channel disguised as convenience. The association between phone-based applications and predatory lending is not theoretical. It is learned from experience.

Banks should read this data as a constraint, not a challenge to overcome. Voice AI can assist with application pre-qualification, document collection, and status updates, but the actual application decision should remain a screen-based interaction. SMS and email are better channels for sending application details that consumers need to review at their own pace. Voice AI in banking works where the conversation is the output. It fails where the conversation is the input to a decision the consumer needs time to make.

Key Takeaways

- Urgency is the only driver of majority acceptance. Fraud alerts (46.7% agree) are the sole question where the benefits of AI voice are immediate and personal. When the alternative to answering is financial loss, skepticism recedes.

- Trust follows a gradient, not a binary. The descent from 46.7% (fraud alerts) to 27.6% (applications) tracks the shift from reactive to advisory to autonomous. Each step away from urgency and toward delegation costs agreement.

- Disagreement hardens as stakes rise. Strong disagreement climbs from 16.2% (fraud) to 29.5% (applications). Consumers are not just unenthusiastic about AI for complex banking. They are actively opposed.

- Voice is a conversation tool, not a decision tool. The application question exposes the medium's limit. Financial commitments require deliberation, comparison, and review. Voice is ill-suited to tasks where the consumer needs to re-read and reconsider.

- Authentication is a trust gateway, not a given. At 31.4%, voice login does not clear the bar for majority acceptance even though it is the simplest task. If consumers will not use voice to log in, they will not use it for anything else until that barrier falls first.

Strategic Implications

For banks evaluating Voice AI, the data points to a narrow but defensible entry point: fraud response. It is the only use case where consumer acceptance is net positive, the business case is immediate (reduced fraud losses, faster resolution), and the infrastructure requirements are well understood. Branded calling to establish caller legitimacy, speech-to-text for accurate transaction detail capture, and carrier-grade reliability to ensure the call connects when the customer answers.

The deployment sequence from here should follow the trust gradient observed in the data. After fraud alerts, the next layer is low-stakes information retrieval: balance checks, payment confirmations, transaction history. These tasks involve reading data, not acting on it. The error risk is minimal because the consumer can verify the information visually after the call.

Transactional assistance (bill payments, transfers) requires a fundamentally different design approach. The 50.5% disagreement rate means the default assumption must be distrust. Every transaction needs explicit confirmation, a clear undo path, and a seamless escalation to a human agent when the customer hesitates. Low-latency voice matters here: any perceptible delay in a confirmation flow feels like the AI is thinking, which erodes confidence.

Recommendations and applications should be the last use cases deployed, not the first. The trust deficit is structural, not technical. Better AI will not fix the perception that bank recommendations serve the bank, or that voice-based applications pressure consumers into hasty decisions. Banks that sequence Voice AI deployment to match consumer readiness, starting with urgency and expanding to autonomy, will see higher adoption than those that attempt a full-channel transformation before trust is established.

Methodology

This survey was conducted as part of the Telnyx Consumer Insight Panel. Data was collected from 105 US adults via SurveyMonkey using a five-point Likert scale (Strongly Agree to Strongly Disagree). All questions were answered with zero skips. Results have not been weighted.

Respondent Demographics

Age: The sample skews toward established banking customers. 37.1% are aged 30-44, 33.3% are over 60, and 21.0% are 45-60. Only 8.6% fall in the 18-29 range. No respondents under 18.

Gender: 53.3% female, 46.7% male. No respondents identified as non-binary or preferred not to answer.

Geography: Respondents span all major US regions. Pacific (22.9%) and South Atlantic (15.2%) are the largest cohorts, followed by East North Central (15.2%) and Middle Atlantic (14.3%). Mountain (8.6%), West North Central (9.5%), West South Central (6.7%), East South Central (2.9%), and New England (4.8%) round out the distribution. No respondents from US territories.

Household Income: Broad income distribution with the largest cohort at $50,000-$74,999 (22.9%). $25,000-$49,999 (14.3%) and $75,000-$99,999 (14.3%) are the next largest. Upper income brackets: $125,000-$149,999 (13.3%), $150,000-$174,999 (5.7%), $175,000-$199,999 (7.6%), $200,000+ (3.8%). Lower brackets: under $10,000 (4.8%), $10,000-$24,999 (6.7%). 3.8% preferred not to answer.

Device: Mobile-dominant. Android phones/tablets (46.7%) and iOS phones/tablets (32.4%) account for 79.1% of respondents. Windows desktop/laptop (13.3%) and macOS desktop/laptop (7.6%) make up the remainder.

Methodology Disclosure Statement

Percentages are based on all respondents unless otherwise noted. These results are intended to provide indicative insights consistent with the AAPOR Standards for Reporting Public Opinion Research. This survey was conducted by Telnyx in June 2026. Participation was voluntary and anonymous. Because respondents were drawn from an opt-in, non-probability sample, results are directional and not statistically projectable to the broader population.

Survey Title: Voice AI Agents for Banking Consumer Perception Study Sponsor / Researcher: Telnyx Field Dates: June 2026 Mode: Online, self-administered questionnaire Language: English Sample Size (N): 105 Population Targeted: Adults with internet access who voluntarily participate in online respondent pool Sampling Method: Non-probability, opt-in sample; no screening or demographic quotas applied Weighting: None applied Questionnaire: Available upon request and after proper internal legal release process and confirmation

Share on Social